Charity Statement of Recommended Practice (SORP)

Simple, Compliant Charity SORP Accounting on Salesforce

Aedon.Accounting helps charities meet SORP requirements effortlessly with clear reporting, strong audit trails and automated workflows – all inside your existing Salesforce environment.

With SORP compliance often complex and time-consuming, Aedon.Accounting gives charities a clearer, simpler way to record, allocate and report financial information – without spreadsheets, manual adjustments or external tools.

Designing a Multi-Dimensional Chart of Accounts for the Charity SORP

Download the whitepaper today

Designed to make SORP compliance easier, faster and more accurate

Aedon.Accounting for Charity SORP

The Charity Statement of Recommended Practice (SORP) provides the framework that UK charities must follow when preparing their annual accounts. It ensures financial statements are transparent, consistent and comparable across the sector.

Aedon.Accounting captures and structures your financial data in a way that naturally aligns with Charity SORP, giving you:

Charity SORP: The Challenges vs. The Solution

A look at where charities struggle – and how Aedon.Accounting resolves each issue.

SORP compliance can quickly become complex, especially when data is spread across spreadsheets, fundraising tools and legacy finance systems.

This comparison shows how Aedon.Accounting simplifies the key problem areas and supports every SORP reporting format, all within Salesforce.

Why Charities struggle with SORP Compliance?

Charity finance teams often face challenges such as:

Aedon.Accounting resolves these issues by bringing finance and operational data together in Salesforce.

How Aedon.Accounting supports Charity SORP account formats

Whether your charity prepares SORP (FRS 102) accounts, Receipt & Payment accounts, or Accrual-based financial statements, Aedon.Accounting provides the structure and reporting tools to handle all required disclosures, categories and notes.

This includes:

SORP requirements aren’t difficult – but the systems charities use often are. The above comparison highlights the typical problem areas and demonstrates how Aedon.Accounting supports compliant reporting formats with less effort, fewer errors and better visibility.

Isn’t it time you considered A NEW WAY OF WORKING.

Useful Resources

The Charity SORP – Your Questions Answered

Navigating the complexities of the Charity SORP can be challenging, but we’re here to help.

Below, we’ve answered some of the most common questions charity leaders and finance professionals ask about SORP compliance and reporting.

The Charity Statement of Recommended Practice is mandatory for all charities – regardless of size. It is a 200-page A4 document of additional reporting requirements that are layered on top of FRS 102.

Unfortunately, and unintentionally, the SORP is ambiguous and poorly written. Complying with the SORP creates financial reports which are overly complex and fail to inform the normal reader.

But that does not matter, although you may not like the SORP as a charity treasurer or advising accountant, you must comply with it. Sorry.

However, help is at hand. We are publishing the “The Plain English Guide to Implementing the Charity SORP” at the end of the year with a RRP of £20.

Yes! There are some minor changes in the Trustee’s Report for “small” charities which are defined as those with a gross income of less than £500,000 for UK charities or €500,000 for Irish.

The aim of the Financial Reporting Council is “to promote transparency and integrity in business”. With regards to charities the aim is to help readers understand three things in particular:

- What are the objectives of the charity?

- What activities does it undertake to achieve those objectives?

- How are those activities funded?

Unfortunately, it only partially meets those objectives. The list of requirements for the Trustee’s Report ensures a comprehensive narrative that explains the first objective of what the charity is trying to achieve and allows for a good description of the activities.

The financial statements are overly complex and unhelpful. The Statement Financial Affairs is the most important report in the SORP and is equivalent to a Profit & Loss Account with a summary balance sheet added at the end. Even experienced readers of accounts find it difficult to judge whether the charity is succeeding or failing.

The SORP was created by some very clever and very experienced accountants, who were probably too clever and too experienced to recognise that what they had produced was far too complicated for charities many of whom rely on unqualified volunteers to fulfil their financial roles.

Even for experienced accountants the SORP is very daunting and made even more so by the ambiguities and problems in its construction.

The SORP is extremely difficult to implement properly unless you have a multi-dimensional accounting system like Aedon.Accounting.

Most charities use starter packages which have a business-oriented chart of accounts that might allow for different departments or cost centres, but certainly don’ support the three-dimensional need to record the nominal code, fund and activity on all purchases. These simpler packages are simply not sophisticated enough to make compliance with the SORP easy.

However, help is at hand. We are publishing the “The Plain English Guide to Implementing the Charity SORP” at the end of the year with a RRP of £20.

The SORP is extremely difficult to implement properly unless you have a multi-dimensional accounting system like Aedon.Accounting.

Most charities use starter packages which have a business-oriented chart of accounts that might allow for different departments or cost centres, but certainly don’ support the three-dimensional need to record the nominal code, fund and activity on all purchases. These simpler packages are simply not sophisticated enough to make compliance with the SORP easy.

However, help is at hand. We are publishing the “The Plain English Guide to Implementing the Charity SORP” at the end of the year with a RRP of £20.

Three-dimensional accounting simplifies the implementation of the Charity SORP.

On every type of income (sales invoice) you record not only the classification of the income using the nominal or general ledger code for that income type, but also the fund that it goes into.

Then, for every purchase invoice you record not only they classification of the expenditure using the nominal code, but you record the activity it was spent on and the fund that is being used to pay for it.

In system terms you record the classification of the income or expenditure using the nominal codes, and then use the Fund analysis code to manage the balance in the fund and the Activity Analysis code to identify which activity is being supported.

Recording this extended information, which is necessary to comply with the Charity SORP, is simple with Aedon.Charities.

The Statement of Financial Activities is the charitable equivalent of a Profit & Loss report for ordinary businesses, which is extended by including balance sheet information for the movement in the funds.

It uses standard classifications of income and expense which are intended to assist with the comparison of different charities.

However, these classifications are then divided according to the different funds which they were paid out of making the whole report far too complex to read easily.

If the SOFA were an Olympic dive, it would have a degree of difficulty of 4.9 out of 5!

Charities are not businesses and therefore create surpluses or deficits in their income and expenditure. These are accumulated year on year as fund, which are also described as reserves.

Under the Charity SORP the surpluses and deficits are recorded against each fund and then accumulated in the same way in the accumulated funds or reserves.

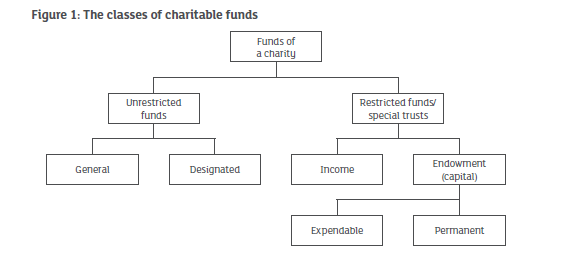

There are essentially two classes of fund: Unrestricted and Restricted.

Unrestricted funds can be applied for any of the charity’s activities. When they are set aside for a specific purpose, they are called Designated. The undesignated funds are called General.

Restricted Funds can be either Income Funds or Endowment Funds. Income funds can be spent in full on the activities defined by the donor. Endowment funds hold capital that can provide an income to be used for the charitable activities.

The Endowment funds are further divided into Permanent Endowments which are held indefinitely or Expendable Endowments in which the capital can be spent at the discretion of the trustees.

The SORP uses this diagram to explain the different types of funds.

The Charity’s activities are the means of achieving its charitable objectives. They are defined in the Trustee’s statement.

Unfortunately, although the initial definition is clear, the SORP then proceeds to use the term activity to also define the different classifications of income expenditure in a a very confusing manner.

It would have been much easier if they had used a different term such as “Classification”. This is how we define the different dimension axes that are necessary to comply with the SORP in what we refer to as 3-Dimensional Accounting.

There are 21 Tables in the SORP and 2 figures. That is the bad news. The good news is that most don’t apply to most charities. The important ones are highlighted below.

| Table | Title | SORP Page |

|---|---|---|

| 1 | Outline summary of fund movements | 28 |

| 2 | Statement of financial activities | 38 |

| 3 | Analysis of expenditure on charitable activities | 48 |

| 4 | Analysis of support costs | 75 |

| 5 | Balance sheet | 83 |

| 6 | Analysis of opening and closing carrying amounts | 89 |

| 7 | Common basic financial instruments | 99 |

| 8 | Statement of cash flows | 115 |

| 9 | Reconciliation of net income/(expenditure) to net cash flow from operating activities | 116 |

| 10 | Analysis of cash and cash equivalents | 116 |

| 10a | Analysis of changes in net debt | 117 |

| 11 | Minimum requirements for a summary income and expenditure account | 120 |

| 12 | Analysis of grants | 124 |

| 13 | Analysis of charitable activities | 125 |

| 14 | Analysis of heritage assets | 135 |

| 15 | Summary analysis of heritage asset transactions | 137 |

| 16 | Example of the disclosure of a toral return approach to investment of permanent endowment | 143 |

| 17 | Analysis of fund movements for a pooling scheme | 153 |

| 18 | Analysis of principal SoFA components for the current reporting period | 173 |

| 19 | Analysis of principal SoFA components for the previous reporting period | 173 |

| 20 | Analysis of net assets at the date of merger | 173 |

| Figure | ||

|---|---|---|

| 1 | The classes of charitable funds | 22 |

| 2 | Guide to accounting for charity combinations | 156 |

There are 29 modules in the SORP. And they are in a somewhat random order! That is the bad news.

The good news is that for most charities there are 6 which are particularly important and these are highlighted below. The others you may need to refer to according to your specific circumstances.

| Module | Title | SORP Page |

|---|---|---|

| Core Modules | ||

| 1 | Trustees’ annual report | 12 |

| 2 | Fund accounting | 22 |

| 3 | Accounting standards, policies, concepts and principles, including the adjustment of estimates and errors |

29 |

| 4 | Statement of financial activities | 37 |

| 5 | Recognition of income, including legacies, grants and financial income | 50 |

| 6 | Donated good, facilities and services, including volunteers | 60 |

| 7 | Recognition of expenditure | 65 |

| 8 | Allocating costs by activity in the statement of financial activities | 72 |

| 9 | Disclosure of trustee and staff remuneration, related party and other transactions | 76 |

| 10 | Balance sheet | 82 |

| 11 | Impairment of assets | 98 |

| 12 | Analysis of grants | 105 |

| 13 | Events after the end of the reporting period | 109 |

| 14 | Statement of cash flows | 111 |

| Selection 1: Special Transactions relating to charity operations | ||

| 15 | Charities established under company law | 118 |

| 16 | Presentation and disclosure of grant-making activities | 122 |

| 17 | Retirement and post-employment benefits | 127 |

| Selection 2: Accounting for special types of assets held | ||

| 18 | Accounting for heritage assets | 131 |

| 19 | Accounting for funds received as agent or as custodian trustee | 138 |

| Selection 3: Accounting for investments | ||

| 20 | Total return (investments) | 141 |

| 21 | Accounting for social investments | 145 |

| 22 | Accounting for charities pooling funds for investment | 152 |

| Selection 4: Accounting for branches, charity groups and combinations | ||

| 23 | Overview of charity combinations | 155 |

| 24 | Accounting for groups and the preparation of consolidated accounts | 157 |

| 25 | Branches, linked or connected charities and joint arrangements | 164 |

| 26 | Charities as subsidiaries | 169 |

| 27 | Charity mergers | 170 |

| 28 | Accounting for associates | 174 |

| 29 | Accounting for joint ventures | 177 |

| Appendices | ||

| 1 | Glossary of Terms | 181 |

| 2 | The Charity Accounting (SORP) Committee | 194 |

| 3 | Thresholds for the UK and the Republic of Ireland | 195 |

| 4 | Basis for conclusions | 197 |

“Aedon is a reliable and powerful accounting solution for any business, thanks to its seamless integration with Salesforce, user-friendly interface, robust reporting features, and top-notch security measures.”

Daniel Ruthenberg, Account Director at Manras Technologies

Why Charities Choose Aedon.Accounting

Charities often battle with fragmented data, inconsistent fund tracking and time-consuming SORP reporting. Aedon.Accounting removes these barriers by bringing finance, fundraising and operations together in one structured, Salesforce-native platform.

What others are saying

Customer reviews

Aedon.Accounting combines CRM and finance to drive down costs and increase revenues PLUS all the customisation that Salesforce enables. Learn more on our Salesforce AppExchange page.

These are all genuine customer experiences shared by users of Aedon.Accounting on our Salesforce AppExchange page. Click below to learn more.

Discover How SORP Becomes Simpler

See Aedon.Charities in Action

After the demo, you’ll have a clear understanding of how Aedon.Charities handles fund accounting, SORP reporting, disclosures and real-time dashboards inside Salesforce. You’ll see exactly how the platform reduces manual work, eliminates spreadsheets, improves audit readiness, and gives trustees and leadership the clarity they need – all while simplifying year-end and strengthening financial governance across your charity.